This FAQ page is updated frequently with new entries. Do you have an additional question you would like answered? Contact us.

Override

What is an override?

A Proposition 2½ override is a voter-approved measure in Massachusetts that allows a municipality to permanently increase its property tax levy beyond the annual 2.5% cap set by state law. It provides funding for recurring municipal operating expenses or services, requiring a majority vote in a local election. Learn more at Mass.gov.

Is this override permanent?

Yes, a Proposition 2½ operating override in Massachusetts is a permanent increase to a municipality's levy limit. When voters approve an override, the additional tax amount becomes part of the base for calculating future years' tax limits.

In Brookline, we have had overrides in 1995 ($2,960,000), 2008 ($6,200,000), 2015 ($7,665,000), 2018 ($6,575,425), 2024 ($11,983,367), and now, in 2026 ($23,250,000).

| Fiscal Year | Vote Date | Result | Yes Votes | No Votes | Department | Description | Amount |

|---|---|---|---|---|---|---|---|

| FY1995 | 5/3/1994 | Passed | 5,958 | 5,072 | General Operating | General Expenditures | 2,960,000 |

| FY2009 | 5/6/2008 | Passed | 5,236 | 4,305 | General Operating | Funding School, Police, Fire, And Library Depts. Etc | 6,200,000 |

| FY2016 | 5/5/2015 | Passed | 6,325 | 3,958 | School | Fund additional enrollment In Brookline Public Schools and expenditures in Municipal Departments | 7,665,000 |

| FY2019 | 5/8/2018 | Passed | 5,412 | 2,371 | School | Funding the cost of expenditures in the Public Schools | 6,575,425 |

| FY2024 | 5/2/2023 | Passed | 7,516 | 4,799 | General Operating | Question 2a Operating Override | 11,983,367 |

See the Commonwealth of Massachusetts Proposition 2 ½ Operating Override database

How much is this override?

This override is unprecedented in Massachusetts history. Ballot Question 1 seeks voter approval for a $23,254,439 override. Of this amount, $17,944,439 is allocated to the Public Schools of Brookline's operating budget, while the remaining $5,310,000 is designated for the Town's municipal operating budget.

This override surpasses the largest in the Commonwealth's history, exceeding the $11,983,367 override approved in 2023 by more than double.

Calculate how much your Real Estate Tax Bill will increase with this override.

Is this override too high?

We believe so. Check out this page in the Community Impact section.

In its Final Report, the Expenses and Revenues Study Committee (the "E&RSC") urged the Select Board to reduce the override amount. They concluded that there were substantial savings that could be realised and additional revenue that could be generated. They argued that the amount of the override should be reduced to take suggested savings and additional revenues into account.

On the savings side, the E&RSC highlighted two areas in particular. These are subject to collective bargaining, which is now underway.

First, it noted that Brookline's percentage contribution to the medical benefits of its employees, at 83%, is high when compared to similar districts.

Secondly, it concluded that School Department teacher salaries are higher than those of similar districts, and are increasing at rates well above the rate of inflation.

Rebalancing these excesses to bring Brookline into line with similar districts would save millions of dollars each year and would substantially reduce the need for and amount of any override. The E&RSC stated that these excesses are "unsustainable" without constant overrides and urged the Select Board not to accept them as "givens" in projecting the funding gap. But the Select Board did not take this advice and approved the full amount requested.

Passing this massive override now will simply sustain the unsustainable, until the next big override, just three years from now.

But rejecting this override will send a message to our town and school officials, including those now engaged in collective bargaining, that the status quo is unacceptable. Changes should be made, and the savings and additional revenues taken into account, before coming back to taxpayers yet again.

Is an operating override the same as a debt exclusion?

No. A Proposition 2½ override is not the same as a debt exclusion. An override permanently increases the tax levy to fund ongoing operating expenses, whereas a debt exclusion provides a temporary tax increase used solely to repay bonds issued for capital projects. Both require voter approval to raise property taxes beyond the 2.5% annual limit.

Brookline will collect an additional $35,379,833 in property taxes for existing debt exclusions in FY 2027 (10.1% of the total amount of the tax levy). In Fiscal Year 2026 the Total General Fund Outstanding Debt is 650,482,815 of which 545,349,140 is exempt (Debt Exclusions) and 105,133,675 is non-exempt. For FY2027, the total Debt Service is $45.7 million. That is $723 debt service per capita.

See the Town's FY2027 Financial Plan Section VII Capital Improvement Plan for more information.

What is the real cost of this override?

This proposed override - even phased in over three years - is a permanent increase of $23.25 million to our property tax base.

That makes it an “incremental” tax that carries on forever into the future that would otherwise not have been collected. Neglected in the conversation is what this represents today in terms of “present value.”

The term “present value” refers to a well established financial concept that is used to calculate the value today of a set of cashflows that extend into the future.

Using a discount rate of 3%, which is the rate at which Brookline is able to borrow, the present value cost of this override is almost $200 million! (Even with a discount rate of an extraordinarily and unrealistically high 10%, the present value cost would be close to $140 million.)

Said another way, by asking for a permanent increase in the tax base of $23.25 million - even phased in over three years - it’s effectively the same as asking tax payers for $200 million today.

We should be clear about the huge tax increase this override really represents.

What is the Expenditures and Revenues Study Committee and where can I read the Final Report prepared for the Operating Override recommendation?

The Expenditures & Revenues Study Committee (E&RSC), appointed by the Select Board with support from the Town Administrator, Superintendent of Schools, and Finance Department, was tasked with analyzing Brookline's projected budget for FY2027 and beyond. The committee's work included identifying structural budget gaps, evaluating expenditures and revenues for efficiencies, exploring alternative funding sources, and updating benchmarks against comparable municipalities. It was also charged with recommending whether an operating override should appear on the May 2026 ballot, specifying the proposed tax increase, fund allocation between the Public Schools of Brookline (PSB) and other Town departments, and supported programs. Additionally, the E&RSC assessed the impact of potential revenue or cost changes on the community, provided guidance on monitoring recommendations, and analyzed the consequences if its proposals were not adopted or approved by voters.

You can find the full report of the ER&CS here.

Did the E&RSC recommend other options, in addition to the one voted by the Select Board ($23.25 million), for the ballot question?

Yes. The E&RSC presented the Select Board with three possible approaches for an override ballot question. Options 1 ($23.25M) and 2 ($18.6M) each involve a single-question ballot, differing only in the total override amount and how it would be raised. Option 3, by contrast, introduces a tiered ballot structure, allowing voters to choose whether to fully fund, partially fund, or decline the proposed override. The E&RSC ultimately recommended Option 3, citing its ability to provide voters with the greatest level of choice. The Select Board ultimately chose Option 1 ($23.25M).

Below is a summary of the three options as outlined in the E&RSC Final Report (pages 8–13):

Option 1: Place the full combined override request of $23.25 million on the ballot, consisting of $5.31 million for Town Services and $17.94 million for Schools. This approach would result in an incremental tax levy increase of 6.99% over three years, with funds raised according to the schedules proposed by the Town and Schools.

Option 2: Front-load the tax levy increase in FY27 while still covering the full FY27–FY29 funding gap for both the Town and Schools. This option reduces the total override amount to $18.6 million, with a 5.59% incremental tax levy increase over three years. The higher initial revenue would exceed immediate needs, with the surplus placed into an interest-bearing stabilization fund for future use.

Option 3: Introduce a tiered ballot question that gives voters multiple funding choices. This structure could be applied to either Option 1 or Option 2. Under this approach, voters would be able to select full funding, no funding, or one or more intermediate levels. The committee recommends that any tiered structure be designed neutrally to ensure voters are presented with clear and meaningful choices.

I am a renter, so why should I say "no" to this override?

As stated in the E&RSC Community Impact section (Page 12), renters are not immune from property tax increases, since the standard Greater Boston lease includes a clause allowing increased property taxes to be passed on directly to renters. In fact, renters in two- and three-family buildings are highly likely to be affected by an override, since tax increases on the building must be borne by a smaller number of units and since the rental units are not eligible for the residential homeowner exemption.

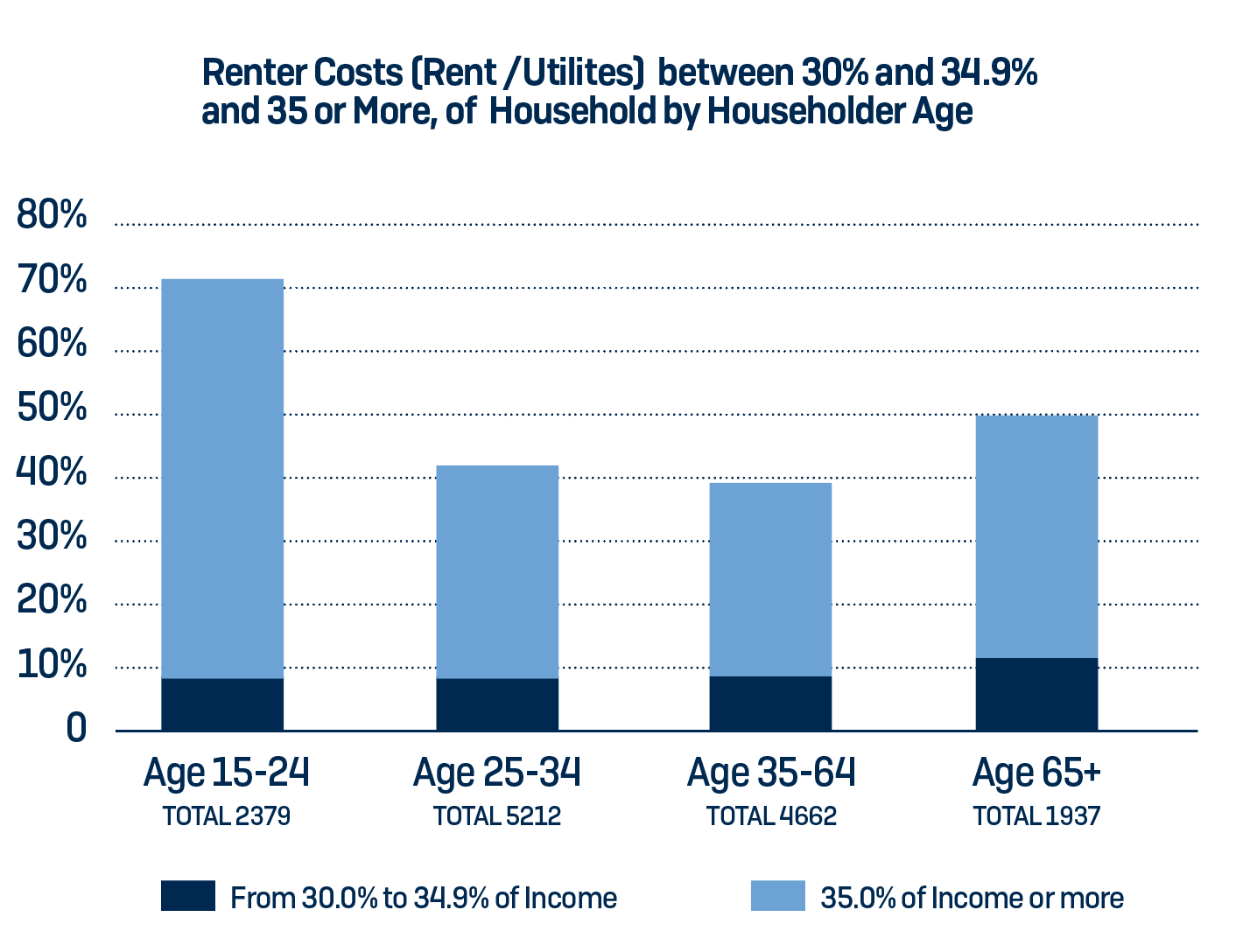

Over 6,650 renters (almost 47%) paid more than 30%, and over 5,300 (37.6%) more than 35%, of their household incomes for housing. The most senior Brookline renters faced the greatest burdens. One-half (49.9%) of senior renters — almost 1,000 — pay more than 30% of their incomes for rent and utilities, with over 700 (38%) paying more than 35%.

Source: E&RSC Final Report

If we vote "No" on the Override, what will happen to Public Safety in Brookline in the near future?

Very little. We will continue to have the excellent public safety services we are accustomed to. The Police and Fire Departments are level funded in Fiscal Year 2027 (July 1, 2026 - June 30, 2027):

The Police Department budget is decreasing by less than 1%. The budget is receiving increased funding for police services, training, equipment and supplies, offset by the reduction of a civilian clerical worker. No police officer positions will be lost.

The Fire Department budget is increasing by 1%. The budget is receiving increased funding for salaries, turnout gear and equipment. The fire prevention division will be reduced by one professional administrative position. No fire suppression personnel will be lost.

This is responsible budgeting. If we vote "no" on the override, the Police and Fire Departments are fully budgeted in FY27. In future years, a hard look will be needed to determine where other departmental budgets can be trimmed, responsibly and without compromising public safety in Brookline.

For more information on these and other departmental budgets, see Brookline's FY27 Financial Plan, available here:

Is it true that if the override does not pass, six police officers would be taken off the street and a fire station would close?

No. The six Police Department positions referenced are currently vacant and have not been filled for the past three fiscal years. During the Advisory Committee's review of the FY2027 Police Department operating budget, the Police Chief stated that current staffing levels are adequate and that public safety services would remain unchanged.

Similarly, during the Advisory Committee's review of the FY2027 Fire Department operating budget, the Fire Chief confirmed that there would be one reduction in personnel, regardless of the override results. In future years, the elimination of a fire company would be considered only as a last resort, as it would disproportionately affect service coverage in a particular area of the town.

Given these facts, including public safety as a central justification for a large override raises concerns. Framing the issue in this way may place undue pressure on voters by tying essential services to a broader funding decision.

Would a failed override be "catastrophic" for our schools, as some are claiming?

We think not, if school leadership and the School Committee act responsibly.

We are being told that a failed override will be catastrophic for our schools. Some of the consequences suggested by school leadership: elimination of middle school conservatory and world languages in 2027; mass firings of teachers; unacceptable increases inclass sizes; etc.

But these are choices that assume a continuation of the status quo. As the Expenses & Revenues Study Committee has aptly stated, this must not be accepted as a "given" but needs to be changed. And they have some suggestions:

- Negotiating better contracts with the unions on contributions to benefits and salary structure and salary increases could save millions of dollars a year. Brookline is out of line with comparable districts in these areas. The negotiations are now underway. See community impacts section.

- Deploying BHS teachers more efficiently might save about a million dollars a year. See pages 54-55 of the Report.

- Examining very deeply the tuition charged for BEEP, so that it can cover its costs and achieve break-even. See pages 79-87 of the Report.

- Renting out space in our new beautiful schools and other Brookline facilities that we are not fully using. See pages 73-78 of the Report.

- Seeking funding for the unreimbursed cost of up to $4m per year to provide special education services to students who are not residents of Brookline. See pages 73-78 of the Report.

- Spreading over several years the $2m cost of replenishing the already ample circuit breaker reserve fund instead of concentrating it all in 2027. If this were deferred entirely to later years, the 2027 budget gap of $4.45m wouldbe cut by $2m, or 44%. This alone would cover the cost of middle school conservatory by a very wide margin.

In addition, there are likely significant opportunities for savings through further review of central office and other non-teaching staffing levels.

So, there are a number of possibilities to avoid catastrophe if the override fails. There are savings to be made and revenues to be generated that could avoid the most damaging of the cuts being proposed by school leadership.

And remember, the School Committee has yet even to consider, let alone approve, ANY of the cuts being proposed, so they are not fait accompli, though that is how they are being presented.

If the override fails, the School Committee will need to reconsider the 2027 budget and, if it acts responsibly, will ask school leadership for a menu of options, as it did last year when unacceptable cuts, including middle school conservatory, were proposedand rejected. And with respect to budgets for later years, those will be considered by the School Committee in due course, by which time we will all know better the scope of savings to be realised and new revenues to be generated. If, at that point, a fundinggap remains, a different, likely smaller, override might be proposed, based on a better understanding of the actual outlook rather than the projections we now have, which simply continue an unsustainable status quo.

So do not be afraid to Vote No! A failed override should not be feared, but should be viewed instead as a much needed catalyst for change.

Will it be necessary to cut out middle school conservatory and world languages to balance the 2027 PSB budget if the override fails?

Brookline school senior management ("PSB") is proposing to cut out middle school conservatory and world languages to balance the 2027 budget, if the override fails. We believe this is being proposed to scare parents into supporting the override.

Last year, when the former superintendent proposed to cut conservatory while protecting central office and other non-teaching positions, parents rebelled and the School Committee demanded alternatives. The result? Conservatory was saved, admin and other non-teaching positions were reduced slightly and the students were better off.

Has the School Committee demanded that our current superintendent propose alternatives to balance the budget? No, it has not. Again, we think this is to preserve the illusion that there are no alternatives to these unacceptable cuts.

But, there are alternatives.

PSB's budget gap for 2027 is $4.45m. Here are some ideas, taken in part from the excellent Final Report of the Expenditures & Revenues Study Committee (the "E&RSC").

1. Defer the $2m replenishment of the already ample circuit breaker reserve fund, now concentrated entirely in 2027. Since circuit breaker receipts this year are $1.4m higher than originally expected, there is room to do this. Moreover, replenishment could then be spread over several years as the E&RSC suggested, perhaps five, ten or even twenty, to reduce the future impact on any one year.

Making this adjustment would cut the 2027 budget deficit to $2.45m.

2. Require the main central office departments, the offices of Teaching and Learning ("OTL"), Administration and Finance and Student Services, to reduce staff to save a certain dollar amount in salaries, say $1m. This would require a reduction of perhaps 8-10 positions in total.

Require the eight K-8 schools and BHS to reduce non-teaching staff to save a certain dollar amount in salaries, perhaps another $1m. This would require a reduction of only one or two positions per school.

The impact of these potential reductions could then be weighed by the School Committee against the impact of the proposed elimination of conservatory (seven FTE) and world languages (fifteen FTE).

By way of example, for the central offices, the OTL organization chart in the 2027 budget book lists eight PK-8 and PK-12 "curriculum coordinators." Their salaries probably aggregate to close to $1m. Are they all essential? Are they all more important to students than the seven FTEs or some of the fifteen FTEs who actually teach conservatory and world languages?

Making these savings would reduce the remaining budget gap from $2.45m to $450k.

3. The E&RSC suggested that there may be savings to be realized at BHS by making adjustments to the "4+1" model for deploying teachers. Based on information from PSB itself, the Final Report suggested that this could reduce FTEs by eight, probably saving salaries of close to $1m.

This would more than eliminate the remaining budget gap, without touching middle school conservatory or world languages.

So there ARE ways to make the budget work that do not cut essential parts of the curriculum. Surprising then, that PSB is focusing instead on cutting valuable school programs and the teachers that deliver them directly to students. But, maybe not so surprising. They know that presenting this as a choice between killing these programs and passing the override will lead parents to choose the override every single time. But the choice is a false one — don't fall for it.

Will this override really have a significant impact on a rich community like Brookline?

Yes, it will. Particularly on the many owners and renters who are "housing burdened", including seniors.

Some say: "nearly everyone who lives in Brookline is rich enough to pay more." This is not true.

The Select Board appointed the Expenditures and Revenues Study Committee (the override study committee or ERSC) to make recommendations, understand the context, and detail analyses to the Select Board regarding the proposed override. Let's take a few moments to consider who is being asked to shoulder this $23.25 million override.

FACT: The increase in property taxes in the first year is 8.04% and the three year impact is a whopping 18.27% increase in property taxes. This added to the 93% increase since 2015 in property taxes and the ongoing payments on our $600 million debt, which the Town voted to support in the building of Driscoll, the High School, Pierce, and the purchase of Newbury College, will result in taxes increasing 130% from 2015 to 2029.

But, doesn't everything go up?

Keeping up with inflation is not easy even for people who have solid, well-paying jobs, but if we think about those on fixed incomes, like our seniors, it gets even tougher. Some analysis from the ERSC might surprise you.

FACT: Property taxes on all classes of residential properties in Brookline have far outstripped the rate of inflation. The rate of increase has been in a range of 143%-265% times the rate of inflation, depending on the type of property.

But, aren't people in Brookline rich enough to afford whatever housing they want. That's why they can live here, right? Again, not true.

FACT: A person is considered "housing burdened" when they pay more than 30% of their income for housing, which includes rent, mortgage, taxes, insurance, utilities, but it doesn't include home/condo maintenance

The ERSC found that:

- 47% of renters paid more than 30% for housing

- 38% of renters paid more than 35% for housing

- 50% of senior renters paid more than 30% for housing

- 38% of senior renters paid more than 35% for housing

- 27% of senior owners paid more than 30% for housing

- 23% of senior owners paid more than 35%. for housing

When we stop and take the time to consider what this override means to the 50% of senior renters, the 47% of renters and the 27% of senior owners who are housing burdened, isn't it time to say NO to making their lives harder because Brookline isn't making the choices and changes necessary to live within 3.5% growth/year, which is more than most families have?

If this override fails, will Brookline lose its AAA Bond rating, raising borrowing costs?

This is what some are claiming, but it is highly unlikely, and is just one more scare tactic.

First, some background on bond ratings: they judge a borrower's (in this case, the Town of Brookline's) ability to repay its debts (Brookline has over $600 million in outstanding debt). Our AAA rating is the highest on the scale, representing minimal risk of non-payment for investors. Most Towns in Massachusetts have high-quality bond ratings ranging from AAA-single A. Important factors influencing a rating include: the local economy, the size and wealth of the tax base, and the amount of debt the Town has outstanding. In Massachusetts, voter support for Prop 2 1/2 overrides and debt exclusions is also viewed positively as these allow a Town additional financial flexibility.

However, a bond rating ultimately reflects the cumulative impact of multiple inputs: tax base growth trends, debt/borrowing trends, and liquidity/fund balances, in addition to override results. So, not only is a downgrade upon one failed override unlikely, it is extremely unfair to point at voters considering an override and blame them for a potential downgrade! One could choose any of a number of financial decisions to "blame".

The Town of Marblehead provides some food for thought: since 1982, Marblehead has had 18 failed overrides, most recently in 2022 and 2023; and not one has passed since 2005. Yet Marblehead hangs on to its AAA bond rating. Newton also had a failed override in 2023, yet remains AAA rated. Multiple factors matter.

Moreover, if our rating agencies become concerned, their first step would be to reduce our "stable" outlook to "negative". That happened just a few days ago in Marblehead, because it persistently drew down on reserve funds to balance its budget. Since Marblehead last rejected an override in 2023, that was not the catalyst that led to the change in outlook. By changing the outlook, a rating agency puts a town on notice and gives it time to put its financial house in order, to avoid an actual ratings downgrade.

But what if the Town does get downgraded? What would be the impact on our borrowing costs?

Since Brookline's existing debt is fixed rate, borrowing costs on our outstanding debt would not be affected. For any future borrowing, the interest rate would reflect market conditions at the time, including the Town's current rating, but also considering the interest rate environment and other "technical" market factors. For example, in 2022, the Town was able to borrow at 2.55%, yet our 2025 borrowing resulted in a 4.45% rate, despite the Town being AAA rated in each case, because market conditions had changed. All else equal, a AA rated bond might pay 0.25% more in interest for a 20 year bond. For a $100 million borrowing, this would equate to $250k/year, or less than 0.1% of Brookline's tax base.

Bottom line: A rating downgrade based on one failed override vote is highly unlikely. Moreover, any downgrade would almost certainly be preceded by a change in outlook, providing time to improve the Town's financial position. And if a downgrade were to occur at some point, borrowing costs would remain extremely favorable.

So, don't fall for the bond-rating scare tactics.

What is on the Critical Path to a Balanced Budget with No Overrides?

What will it take to get away from these recurrent overrides in Brookline?

Staff salaries account for 87.5% of the 2027 schools budget. It will be impossible to balance the budget on a sustainable basis without coming to grips with compensation issues.

According to the Town's own E&RSC Report, teacher salaries at virtually all levels of seniority are higher in Brookline than in comparable districts. Moreover, these salaries have increased in many cases much faster than inflation, due to the combined impact of (a) “step” increases for the half of teachers still climbing the ladder of seniority and (b) cost of living adjustments. The Report notes that, in projecting salaries for 2027-2029, Brookline schools management assumed annual increases of 5% on a constant FTE basis. 5% is way above inflation, and also well above the 3.5% generally expected annual increase in regular town revenues, and so further exacerbates the budget problem. The E&RSC also reports that because they did not receive the school budget until two days before their report was due they could not fully evaluate, question, or analyze the projections.

The Report also states that Brookline’s contribution to staff health benefits is 83% of the cost, exceeding that of comparable districts, in many cases by a lot. It identified increases in the cost of health benefits as a main source of budget stress, year after year.

The E&RSC stated explicitly that the schools’ salary structure and salary increases, compounded by Brookline’s high level of contribution to health benefits, are “unsustainable” and should not be accepted as “givens.” Getting these items to the levels of comparable districts would save many millions of dollars each year. Consequently, the E&RSC urged Brookline's Select Board to reduce the amount of the override, but the Select Board chose not to follow this advice, and barely even discussed compensation issues.

So, this override of $23.25m — the largest ever in Massachusetts — is based on projections that assume the perpetuation of compensation structures that the independent experts on the E&RSC warned the Select Board are “unsustainable”.

Collective bargaining is now underway. If the proposed override passes, all the money needed to sustain the unsustainable status quo for another three years will be available, at the expense of overburdened taxpayers. The unions would be foolish not to demand it, and the School Committee could well fear being considered reckless if it were to trigger an illegal strike by threatening to withhold it. The incentives are completely wrong.

To align the incentives properly, this override must be defeated. The School Committee would then be empowered to negotiate fair but fiscally responsible contracts that are more in line with those of comparable districts; and the unions would know that there are real constraints on the availability of resources.

The Select Board failed to act, despite the sound advice of the E&RSC, but you can correct that mistake by voting NO on the override and help put Brookline on a sustainable path.

This is the last chance you will have to fix this problem until the next override: Let your voice be heard this time.

And as you consider this override, and think about these compensation issues and the responsibilities of the School Committee, please take a look at this letter to the Brookline News, which highlights a glaring conflict of interest for the School Committee’s lead negotiator. Say NO to this override, because practices like this undermine all prospects for the fiscally responsible use of your hard-earned money.

VOTE NO!

What??? You Mean Brookline has a Surplus of Revenues?

Yes on 1 Proponents Say: “The Town of Brookline’s finances are in dire shape as costs rise more than revenues! We need to raise taxes again, we have no choice!”

Wait ... wouldn’t that mean the Town runs deficits, or breaks even at best?!?!?

Not even close, because that statement is FALSE. The Town has actually run a very healthy surplus in recent years, despite everything you are hearing about tough times, inflation, and the "need" to increase your taxes even more than is already scheduled (remember, +11% even without the override to fund Pierce debt service, +18% with this override).

From FY19-24, the General Fund (the Town’s main “operating account”) generated the following surpluses: $12.7million, $12million, $5million, $21million, $24million, and $29million respectively. (FY 25-26 audited financials aren’t yet available but results are expected to be similar, according to the FY27 Financial Plan). Source Document: Budget Central / Financial Reports Center | Brookline, MA - Official Websitebrooklinema.gov

So, taxes have gone up 93% since 2015 and the Town is annually collecting more than it needs to spend?!?!

Yes. It is considered prudent financial practice to budget revenues and expenses conservatively and end up with surpluses that can be used to build fund balances, establish “rainy day funds” , and save up for employee retirement costs.

And build we have! Fund Balances have continued to rise, even in the face of cuts to schools and services.

This practice enables a portion of the budget (Free Cash) to fund future capital improvements and contribute to reserves for a “rainy day”. A cut of this cash is called the “Stabilization Fund” and may be appropriated for any municipal purpose, and stands at about $18million.

We recognize the need for the Town to save for a rainy day and save for retirement benefit payments and future capital needs. However, the taxpayer may want to do the same, but climbing rents or property taxes are eating into their household surplus, or worse, forcing household cutbacks.

So, let’s have a conversation with Brookline residents on how, when, and how much of the Stabilization and General Fund Balances to use as we endeavor to broaden revenue sources and right size expenditures over the next several years. And as we consider this, let’s of course bear in mind that maintaining adequate reserves is critical to keeping our triple-A credit rating, which we do not want to put at risk.

Let’s lay out some options and be clear about implications to the Town’s credit profile and credit rating in each scenario instead of asking for $23million, like the Select Board did in this presentation before ultimately deciding NOT to give voters options.

We recognize the prudence of budgeting for surpluses, but we also recognize the tension between doing so and repeatedly asking taxpayers for more instead of prudently deploying the savings they helped generate.

Let the voters decide if the rainy day has arrived! Vote No on Question 1 on May 5th!

Taxes

How do I find out how this override will affect my Real Estate Tax Bill?

The impact depends on your property's assessed value. The Town has created a calculator that allows you to look up your property or enter a value to estimate your potential increase. It will forecast the amount the override will increase your bill for Fiscal Year 2027.

We want to show you the full picture. Our tax calculator below goes a few steps further. It shows you the possible full real estate tax bill that you may receive for FY2027, FY 2028 and FY 2029.

Try our Override Tax Impact Calculator

Here are sample calculations for single family homes.

$1.0M Single-Family Home

| With Override | No Override | ||||

|---|---|---|---|---|---|

| Tax Bill | Prop 2½ & Debt | Override | Tax Bill | Prop 2½ & Debt | |

| FY2026 | $10,240 | $10,240 | |||

| FY2027 | $11,063 | +$520 | +$303 | $10,760 | +$520 |

| FY2028 | $11,582 | +$347 | +$172 | $11,098 | +$338 |

| FY2029 | $12,182 | +$359 | +$241 | $11,442 | +$344 |

| Increases | +$1,942 | +$1,226 | +$716 | +$1,202 | +$1,202 |

| 3-Year Impact | +$4,107 | +$2,580 | |||

Median Single-Family Home ($2.042M)

| With Override | No Override | ||||

|---|---|---|---|---|---|

| Tax Bill | Prop 2½ & Debt | Override | Tax Bill | Prop 2½ & Debt | |

| FY2026 | $20,910 | $20,910 | |||

| FY2027 | $22,591 | +$1,062 | +$619 | $21,972 | +$1,062 |

| FY2028 | $23,651 | +$709 | +$351 | $22,662 | +$690 |

| FY2029 | $24,875 | +$733 | +$491 | $23,365 | +$703 |

| Increases | +$3,965 | +$2,504 | +$1,461 | +$2,455 | +$2,455 |

| 3-Year Impact | +$8,387 | +$5,269 | |||

$3.0M Single-Family Home

| With Override | No Override | ||||

|---|---|---|---|---|---|

| Tax Bill | Prop 2½ & Debt | Override | Tax Bill | Prop 2½ & Debt | |

| FY2026 | $30,720 | $30,720 | |||

| FY2027 | $33,190 | +$1,561 | +$909 | $32,281 | +$1,561 |

| FY2028 | $34,748 | +$1,042 | +$516 | $33,295 | +$1,014 |

| FY2029 | $36,547 | +$1,077 | +$722 | $34,327 | +$1,032 |

| Increases | $5,827 | +$3,680 | +$2,147 | +$3,607 | +$3,607 |

| 3-Year Impact | +$12,325 | +$7,743 | |||

Increases in Tax Bill from 2026. Percentages increase from Town Override FAQ and E&RSC Final Report. Amounts compounded year over year for Prop 2 ½ & Debt. Override increases are calculated from FY2026. Total 3-Year Tax Impact is calculated at the cumulative increase of taxes over the three years of the override with respect to FY2026. In other words: (FY2027 - FY2026) + (FY2028 - FY2026) + (FY2029 - FY2026) = TOTAL 3-YEAR TAX IMPACT

Some are saying that Brookline is a low tax community — is that true?

No, quite the opposite. When analyzed properly, Brookline residents face the highest tax burden in Massachusetts, by far.

The best way to look at residential property tax burden is in terms of the percentage of after-tax income. This is the best measure because residents pay their property taxes out of income, not out of the values of their homes, which are illiquid. Sudden big hikes in property taxes, such as those now proposed in Brookline, are especially difficult for those on a fixed income and for those facing fast-rising healthcare costs. Seniors will be worst affected by the proposed override, which has come on top of a 93% property tax rise in the last ten years.

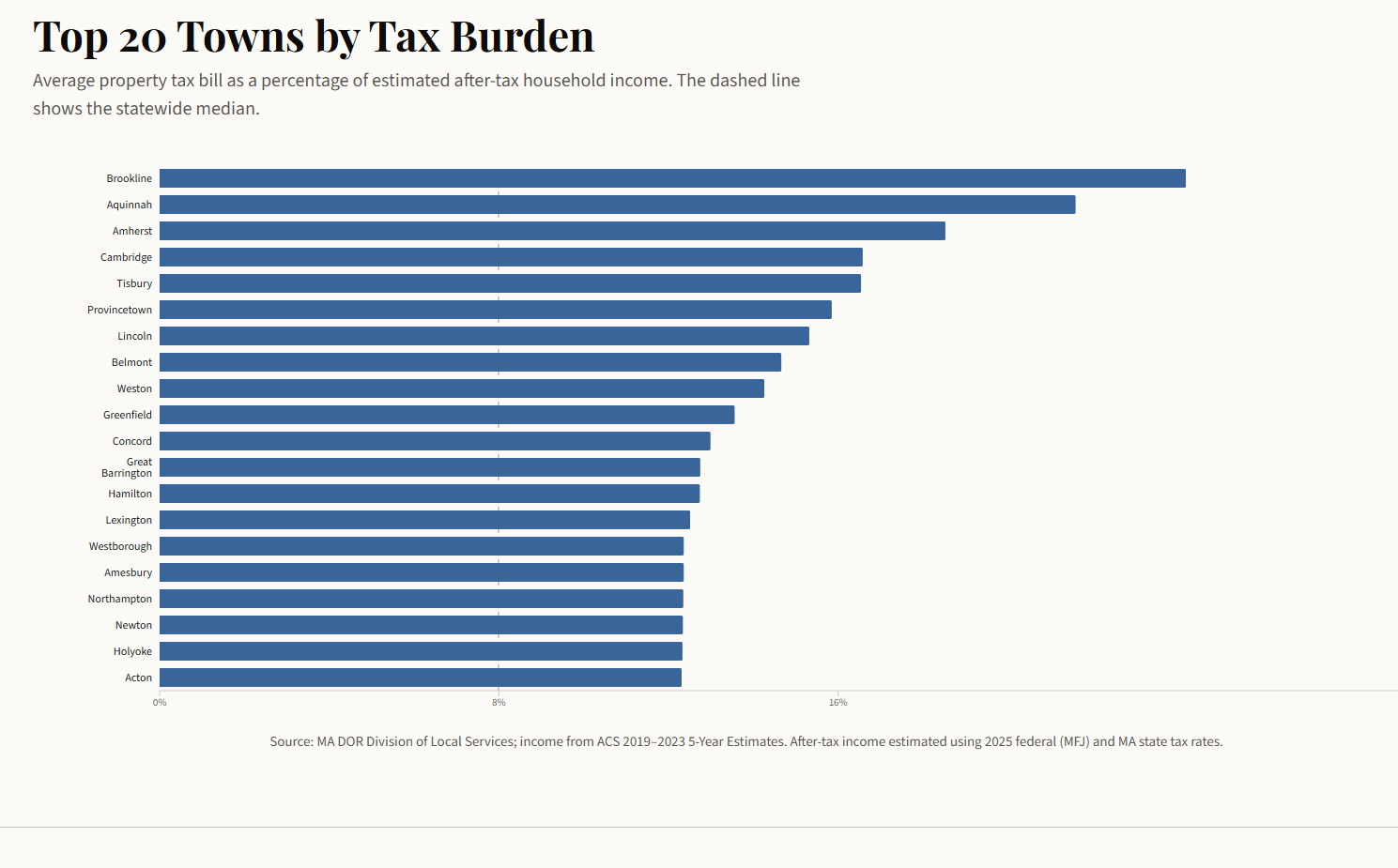

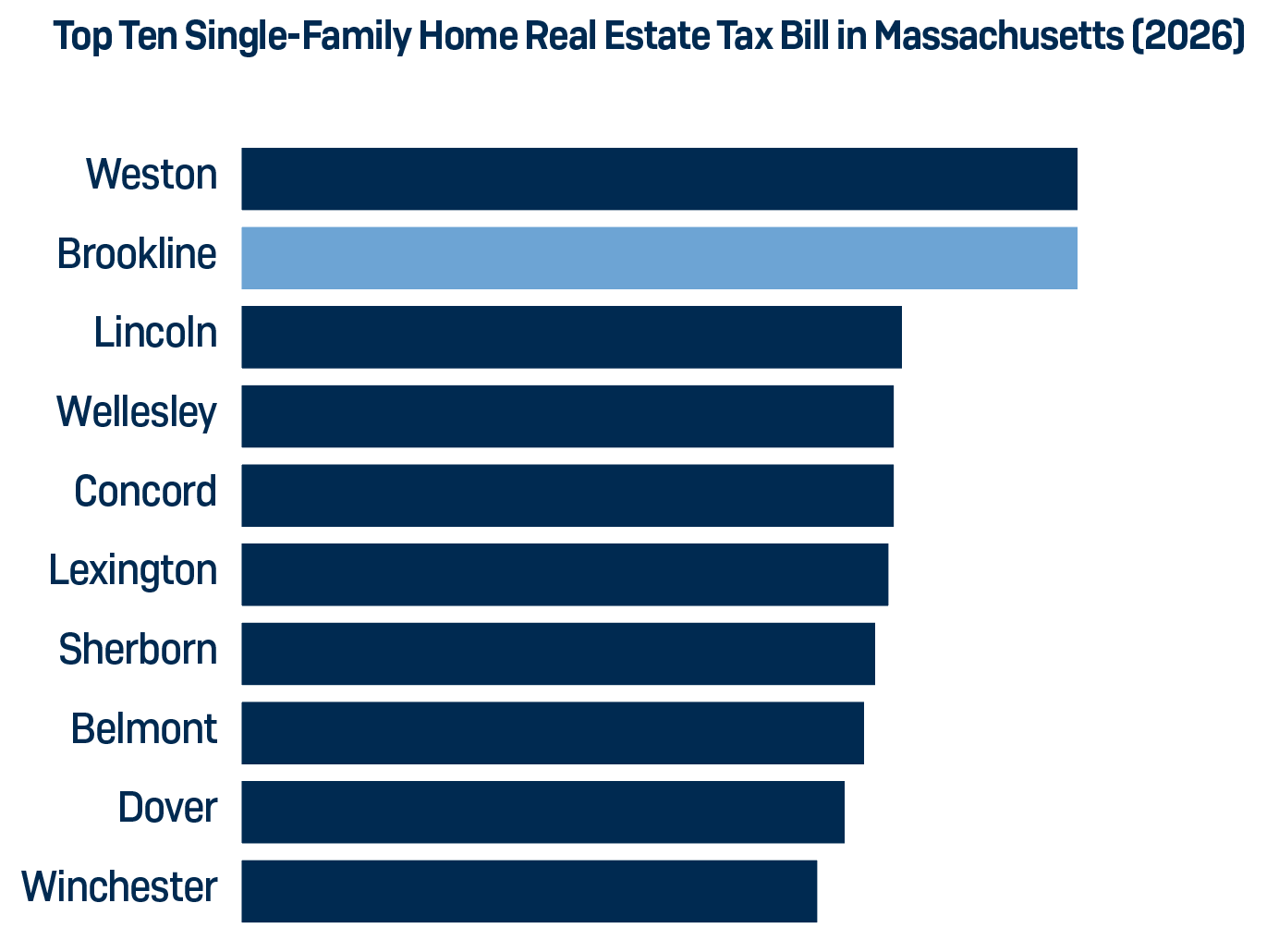

In terms of the percentage of estimated after-tax income used up by property taxes, Brookline is first in the state, by a lot. In terms of average size of bill, we are number 2, just behind Weston.

Looked at another way, Brookline placed 72nd out of 351 communities according to the US Census Bureau American Community Survey (ACS) data from 2023, with a median household income of $140,631, behind Natick, Reading and 69 other towns, including Newton (24/351) at $184,989. The result is that Brookline leads municipalities by far in FY2025 taxes/household when measured as a percentage of gross median household income, at 17.58%.

Will the override cost you just $20/month if you own a $1m home?

No, it will cost you more than three times that!

Those claiming that the cost would be just $20/month appear to be ignoring that the override is phased in over time. As the table above shows, by 2029 the total hit comes to $762.

So, in 2029, the override tax on a $1m home would be over $63/month!

Please also note that the median value of a home in Brookline is about $2m, not $1m. Again, from the table above, by 2029 the total override increase on a median home would be $1,555.

That is about $130/month in 2029!

One more thing: the override also permanently increases the tax base. So, after 2029, future increases will all be calculated off of a bigger number. This is a hidden cost of the override that should not be ignored.

What is a Residential Exemption and who qualifies for it?

The residential exemption reduces the taxable value of your home by a fixed dollar amount. In FY2026, eligible homeowners can deduct $354,974 from their property's assessed value when calculating their tax bill.

This exemption is applied in addition to any other exemptions a taxpayer may qualify for. However, state law requires that a property's assessed value cannot be reduced below 10% of its fair market value.

The exemption is reflected as a credit on the third-quarter tax bill. If you believe you qualify but do not see the credit applied, you must submit a Residential Exemption application to the Assessor.

Any homeowner who owns and occupies a residential property as their principal residence may apply. The property must be used as the taxpayer's permanent home and legal residence as of January 1.

Additional details are available on the Assessor's Office website.

Is Brookline really limited to raising property taxes by 2.5% per year?

No, property taxes have gone up by much more than that, and will continue to do so, even without this override.

In 2023 the Property Tax Levy stood at $281 million. In 2026? 332 million. That's right, Brookline taxpayers have faced massive tax increases, amounting to a staggering $51 million (18%) in just three years.

The burden on taxpayers has grown by more than inflation, sometimes twice as much, since 2023!

HOW? Brookline's total property tax levy by year includes:

- The 2.5% increase

- New Growth — which has typically added 1%

- Operating Override Dollars passed

- Debt Exclusion Dollars

Your taxes have increased in the face of cuts to programs and services and will continue to grow. Another +11% in hikes over the next three years is happening even without this override, due to the phase-in of the 79% increase in annual debt service payments since 2023.

So, don't accept any justification for this override on the basis that 2.5% is simply not enough; the increases have been and will continue to be much greater, even without this override.

Some say Brookline's tax rate is one of the lowest in the Commonwealth, so why are real estate tax bill so high?

Brookline, despite having one of the lowest residential tax rates in Massachusetts (around $10.24 per $1,000 of assessed value in FY 2026), faces a significant challenge with its real estate tax bills. This is primarily due to the town's exceptionally high property values and its heavy reliance on property taxes to fund its municipal services. Property taxes constitute approximately 73% to 79% of Brookline's revenue.

In addition, Brookline voters have frequently approved tax overrides to exceed the limits set by Proposition 2½. These overrides have been particularly instrumental in funding large capital projects, almost three-quarters of a billion for school construction including the ongoing $212 million renovation of the Pierce School.

Brookline's average single-family property taxes (the data provided by the Department of Revenue, or "DOR") increased at a much faster rate than those of communities identified by PSB as similar school communities. Brookline's single family property taxes increased by $12,627 (from $13,610 to $26,237) between FY15 and FY26, or 229% of the median increase of $5,524 in the similar school communities.

And if we look simply at the percentage increase in taxes as reported by the DOR to factor out Brookline's greater property values, Brookline's single-family property taxes increased by 93% versus a 64% median increase in the similar school communities, or a rate of increase 146% that of the comparable communities.

As a result of the combination of high property valuations and the need for substantial revenue generation, Brookline emerges as the second-highest average single-family tax bill in Massachusetts in 2026, with an average tax bill of approximately $26,237.

Source: Mass.gov Division of Local Services. FY2026 Statewide Average Single-Family Tax Bill

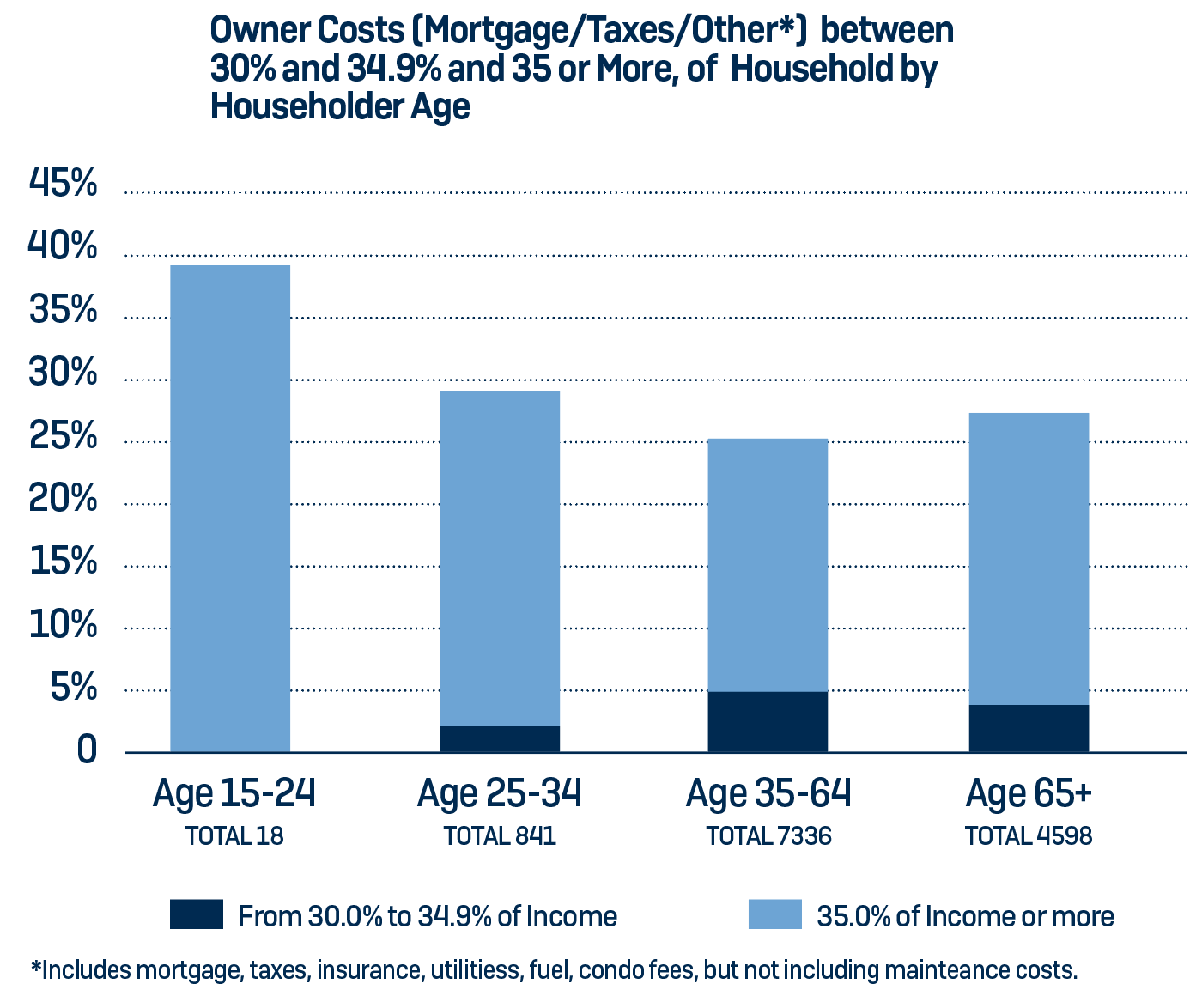

Brookline owners are burdened by housing costs, even without an override further increasing property taxes, with thousands already paying more than 30% and even 35% of their household incomes for housing according to 2024 American Community Survey calculations. The impact is particularly great among seniors age 65 and over.

Over 3,300 owners face housing costs greater than 30% of their household incomes, and 2,800 greater than 35%. This includes 1,250 seniors (27.2% of senior owners) paying more than 30% of their income for housing, and over 1,060 seniors (23.1%) paying more than 35%.

Source: E&RSC Final Report

Voting on May 5

When is the Town election and where do I go to vote?

The Town election is on May 5th, 2026. Polls are open from 7 am to 8 pm.

To find out where you vote, you can visit the Commonwealth of Massachusetts Where do I vote? site for polling information.

How do I register to vote?

Any person is eligible to register to vote if they:

- Are a Massachusetts resident

- Are a United States citizen

- Are at least 16 years old

You can register to vote in different ways.

- Online If you are a US citizen and have a Massachusetts drivers license or state ID, you may register to vote online.

- By Mail You may obtain a mail-in voter registration form from:

- Download the mail-in voter registration form from the Secretary of State.

- Brookline Public Main Library as well as the branch libraries

- United States Post Offices

- Various other locations throughout the state

- In-Person You may visit the Town Clerk's office, located in Brookline Town Hall and complete a voter registration form in person.

Can I vote by mail?

Yes! All registered voters are able to vote by mail. The Town Clerk has provided these links to submit you mail-in ballot.

Last day to request a Mailed Ballot is Tuesday, April 28 by 5PM. Completed Vote by Mail Applications can be submitted to the Town Clerk's office:

- By Mail to Brookline Town Clerk, 333 Washington Street, Brookline, MA 02445

- In-Person at the Town Clerk's office in Town Hall, 333 Washington Street, Brookline, MA Room 104

- Drop Box by dropping it in the one of the Ballot Drop Boxes. Drop Boxes are located at:

- Town Hall, 333 Washington Street, Brookline, MA

- Coolidge Corner Library. 31 Pleasant Street, Brookline, MA

- Putterham Library, 959 West Roxbury Parkway, Chestnut Hill, MA

- By Emailing signed applications to townclerk@brooklinema.gov

Can I vote early in-person?

Yes! All Brookline voters are eligible to vote early in-person for the May 5 election. Voters who requested a ballot by mail and have not returned their ballot may vote in-person during the early voting period.

In-Person Early voting locations and times:

Brookline Town Hall, 333 Washington Street

Saturday, April 25th 10AM-4PM

Sunday, April 26th 10AM-4PM

Monday, April 27th 8:00AM-5:00PM

Tuesday, April 28th 8:00AM-5:00PM

Wednesday, April 29th 8:00AM-5:00PM

Thursday, April 30th 8:00AM-5:00PM

Friday, May 1st 8:00AM-12:30PM

Putterham Branch Library, 959 West Roxbury Parkway

Saturday, April 25th 10AM-4PM

Sunday, April 26th 10AM-4PM

Coolidge Corner Library, 31 Pleasant Street

Saturday, April 25th 10AM-4PM

Sunday, April 26th 10AM-4PM